CONFLICT MINERALS OF TIBET:

#3 IN A SERIES: COPPER GEARS UP BIGTIME AMID COMMODITY PRICE CRASH

This series of blogs highlights the specific minerals extracted from the Tibetan Plateau, despite the protests of Tibetan communities determined to protect their livelihoods, sacred mountains and pilgrimage routes. This series also introduces, to Tibetan readers, the new conflict minerals regulatory regime which effectively bans the entry of conflict minerals into the global commodity supply chain that ends in your hand, in your mobile phone.

THE COPPERBELT ARCHIPELAGO OF SOUTHERN TIBET

When, in 2012, I wrote a book about mining in Tibet, it seemed China’s appetite for minerals was insatiable, having survived the great global recession of 2009 onwards with hardly a blip in demand. By then the global commodity boom had been rolling on nonstop for a decade and nothing, it seemed, could slow it, not even a global financial crisis. And all the long term predictions, based on assuming China can, must and will achieve the same consumption levels of the richest countries, cheerfully forecast decades more of rising mineral extraction worldwide to meet China’s needs.

How wrong we all were. The unstoppable Chinese demand, in the aftermath of the global crash, was fuelled by endless stimulus money pumped in by China’s central authorities, ostensibly for infrastructure construction, which uses up lots of metals and other basic commodities. Much of that money was diverted, often by local governments, to much more profitable real estate ventures, constructing all those tower blocks and ghost cities of empty apartment blocks in the desert. They too needed lots of copper, steel and other metals.

Then the music finally stopped, just after the book, Spoiling Tibet: China and Resource Nationalism on the Roof of the World was launched in October 2013. As well as apartment towers, all that stimulus had built many more smelters and refineries than China, or the world market, actually needed, and suddenly the big new problem was oversupply.

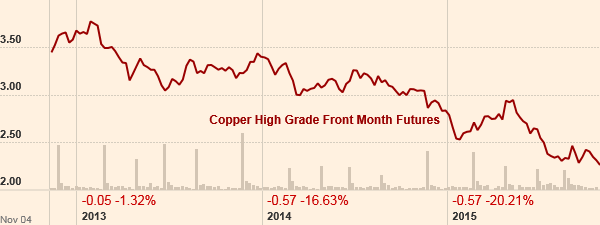

Now, in 2015, that problem is bigger than ever, so big that a major driver of China’s New Silk Road project is to establish expert markets in neighbouring Asian countries for all the excess supply. But prices have fallen sharply, and have now remained low for years, and show no sign in the short term of recovering, even if the long term pundits are right that there is still a long way to go before China uses copper and other metals as intensively as the US.

Until the recent over supply crisis, China’s mining companies, nearly all state-owned, pursued an aggressive strategy of mergers and acquisitions worldwide to get hold of more raw materials, as well as expanding rapidly into Tibet, notably the big copper/gold deposits at Shetongmon near Shigatse, at Kham Yulong between Chamdo and Derge, and Gyama upstream from Lhasa.

Two companies stand out in this rush: Jinchuan and Zijin. Jinchuan has long dominated nickel supply in China. Its home base is far inland, in Gansu, close to the main rail line connecting China and Tibet, placing Jinchuan in the ideal position to be the smelter for the first big copper mine to get under way in Tibet, at Shetongmon. The Canadian company Continental, part of the Hunter Dickinson Group, did much of the work of quantifying the size of the deposit and the most profitable strategy for extracting the copper, gold and silver there. Then Jinchuan bought out not only Continental’s interest in Shetongmon, aided by China’s national rule forbidding foreign investors from actually mining molybdenum (one of Shetongmon’s minerals). Jinchuan went one further and bought Continental, which is now a subsidiary of Jinchuan.

Jinchuan also pressed ahead with constructing a big new copper smelter, just as the prices started tumbling. By April 2014, Jinchuan’s oversupply problems became so acute, they reneged on contracts with their suppliers in far away Chile, relying on the concept of force majeure, meaning uncontrollable disaster, to cancel contracts for Chilean copper concentrates. Jinchuan announced a problem with oxygen supply to the main Gansu smelter, a problem so severe it would knock out all production for as much as four months, giving Jinchuan a breather.

This occurred just as China, at great expense, completed the rail extension from Lhasa to Shigatse, well to the west, leaving only 80kms to the Shetongmon mine. So Tibetan copper, in big quantities, became available, along with supplies from Chile and elsewhere, at exactly the time demand tanked.

That’s a major reason we don’t hear so much about mining it Tibet these days. From the perspective of China’s major mining companies, access to capital isn’t a problem, especially since the stock markets are again booming, and investors are keen to get a slice of the action, despite the overall economic slowdown. The problem is where to invest, where to get the best bang for the renminbi. Tibet doesn’t cut it, compared to the available alternatives.

This brings us to the other company with a major slice of Shetongmon, Zijin Mining, based in eastern China, its fortune built on gold. In 2011 Jinchuan sold a 45 per cent stake in Shetongmon to Zijin, a big company with a strong history of going global. In May 2015 Zijin acquired half of the troubled Porgera copper/gold mine in Papua New Guinea, from a heavily indebted Canadian miner, Barrick. At the same time, Zijin also announced it had bought almost half the Kamoa copper/gold mine in Democratic Republic of Congo from another Canadian miner, Ivanhoe.

Zijin has also acquired mines in Inner Mongolia, Xinjiang, Tuva (the most Tibetan part of Russia) and Kyrgyzstan, a literal embarrassment of riches.

Why, at a time of over supply, depressed prices and force majeure, would Chinese miners want to buy mineral deposits in difficult places like PNG and Congo? This tells us much that is relevant to Tibet. Remarkable as it may seem, mining projects ready to roll, in remote Congo and PNG are actually less remote, less difficult than mining in Tibet, building it all from scratch. Tibet is actually harder.

Much of this is because the Tibetan Plateau is huge, and mineral deposits are often in areas difficult to access. China has spent decades building infrastructure, but there is still so much to be done, especially before the massive copper/gold deposits at Yulong, in precipitous Kham, are ever to be mined, concentrated, smelted and shipped out to lowland Chinese industries.

But there is another reason why Tibet is harder than PNG or Congo: the Tibetans. Although Tibetans feel disempowered by authorities declaring protests to be criminally splittist, they fearlessly persist in protesting against mining, often taking care to quote Xi Jinping’s environmental pronouncements in the biggest possible banner headings. As the eminent Tibetanist scholar Gray Tuttle pointed out recently in article in Foreign Affairs, it takes a state with 1.3 billion population to hold down the Tibetans. That is how Tibetans see it.

While small scale mining is rampant across Tibet, the much more publicly visible, capital-intensive large scale mines in Tibet are taking a long time to develop, longer than one might expect if all those Five-Year Plan announcements of mining as Tibet’s “pillar industry” were to be believed. It is certainly taking longer than I expected when I wrote that 2013 book on mining.

CANADA’S CHINA GOLD INTERNATIONAL AT GYAMA

Longer is not never. Demand may yet rebound, mining is highly cyclical. If China is serious about adopting the American life style and American consumption, the minerals of Tibet will be in demand, especially as China’s biggest manufacturers move far inland, close to Tibet. But not just yet. However, there is one major exception. China Gold International (CGI), China’s biggest gold producer, is now in the copper mining business big time, and is dramatically increasing its extraction of copper (and gold) from Tibet, at exactly the time the world’s biggest copper producers are urgently scaling back production, to save costs, reduce debt and maybe stabilise steadily falling prices.

What is going on? Why would CGI expand at exactly the moment global giants such as Freeport and Glencore are slashing extraction from their existing mines, which are among the biggest, and lowest cost, in the world?

The copper price is in steady decline, not just a temporary blip.

Copper is not like oil. The biggest oil producers, notably Saudi Arabia, can afford to gamble that even if they make little profit when prices are low, those low prices drive higher cost producers out, such as US frackers, Canadian tar sands, maybe even the Russians. It’s a long term gamble that justifies short term pain. Copper, and most metals, are different. There have been so many mergers and acquisitions in recent years that the biggest mining companies are often deep in debt, and know full well that only the fittest survive. So they are ruthless about cutting output, in the hope that supply will slip below demand and prices will rise again.

In late 2015 Glencore slashed zinc production by one third. In October 2015 Freeport, “the world’s largest listed copper producer, said it would cut half of the output from its Sierrita mine in Arizona and was considering a full shutdown. The partial curtailment will take about 100m pounds (or 45,000 tonnes) of copper out of the market annually, as well as 10m lbs of molybdenum.”

So how come CGI chose this, of all times, to announce a massive expansion, as reported in the first of this blog series? Every one of the metals in CGI’s Gyama deposit –copper, gold, silver, molybdenum, zinc and lead- is way down in price and showing no sign of recovery. When everyone else is slashing production, Including China’s own rare earth miners, why is CGI scaling up?

The likeliest answer is simple: CGI is driven not solely by market forces, but also by political forces.

CGI appears to be a Canadian based corporation listed on stock exchanges in Toronto and Hong Kong, that raises its capital expenditure budget from shareholders, like any normal corporation. But CGI has another way of accessing cheap money, from sources more interested in political than financial dividends. CGI can get loans from China’s state owned banks, on highly concessional terms, with generous time allowed to pay back loans that, if the copper selling price stays low, may never be paid back.

CGI’s political patrons are at both national level and also in Lhasa. Both governments badly want CGI to succeed in becoming the first big mine in Tibet, bigger than its only competitor in scale, Shetongmon. To that end, Beijing can, and in October 2015 did, order several state owned banks to lend massively to CGI. These banks, known politely as “policy banks”, did as instructed, even if they had doubts they would ever see their money again. Not only did the big national banks finance this expansion, so too did Tibet Bank. The RMB 4 billion loan (US$627 million) was “led by Bank of China, which acted as the lead manager, as well as with Agricultural Bank of China, China Construction Bank and Bank of Tibet.”

The big banks have recently been targeted by the CCP’s corruption crackdown, which has the explicit aim of bringing them more firmly under Party control. The Party has always hoped Tibet could be made to pay its way, even become a profit centre for China, living up to its reputation as a “treasure house.” That means establishing enterprises capable of generating employment for politically reliable immigrant workers, including the sons and daughters of officials stationed in Lhasa.

For some, the payoff is quick, as the Financial Times reported in 2014: “Misallocation of capital and poor investment decisions are not the only explanation for the enormous waste in China’s economy. A significant portion of China’s post-crisis stimulus binge was simply stolen by Communist Party officials with direct responsibility for boosting growth through investment, according to separate estimates by Chinese and overseas economists.”

This is where Bank of Tibet, and the government of Tibet Autonomous Region come in, the latter (despite being desperately short of locally generated revenue) having offered CGI the further sweetener of a 30 per cent rebate on royalty payments. Within one year of its 2012 opening, the Bank of Tibet’s “loans were made to major infrastructure projects in the rail, hydropower and energy sectors.” Bank of Tibet lends very little to Tibetans.

So it is hardly surprising that this Bank of Tibet would also lend to CGI, whether the loan makes commercial sense or not. But where does this Bank of Tibet get its capital from? Bank of Tibet, from the outset, was a creation of state banks, not depositors. The first announcement, in 2011, explains: “Bank of Tibet, to be registered in Lhasa, will be sponsored by 15 well-known domestic banks and good-performing companies. The bank plans to initially raise CNY 1.5 billion capital and will introduce Bank of Communications as strategic investor.”[1]

This is yet another example of the developmentalist state pumping money into Tibet, in the hope of a political payoff. This becomes obvious if one looks at the detailed business case CGI makes for its future profitability, publicly available due to regulatory filing requirements in Canada. CGI claims it will be profitable, but among the many assumptions built into this forecast are assumptions as to the long term price CGI can expect for the many metals it will produce. CGI’s 2013 business case argues that: “there is potential for higher copper price with improved global growth rates expected in 2014. With this in mind, the long-term forecast copper price of USD 6,393.40/t is deemed reasonable. This value will continue to be used in the economic analysis in this report.”[2] The actual copper price in November 2015 is $5052, with China’s hedge funds continuing to bet it will decline further.

By tonnage of output, copper is by far the biggest product CGI will produce. Gold and silver are minuscule amounts by comparison, but gold will earn as much as eight percent of sales revenue. Gyama is first and foremost a copper mine, with gold and silver the icing on the cake.

CGI makes similarly dubious assumptions about the prices it will get for its other products, gold, silver and molybdenum. If this were a commercially competitive mining company, CGI would, like its global competitors, at the least be holding off investing at this inauspicious low point in the commodities cycle.

CGI’s dependence on Bank of Tibet shows they are both creatures of the developmentalist state. As official media put it, in 2012: “Bank of Tibet, the first regional bank in southwest China’s Tibet Autonomous Region, recently obtained a financial business license from the Tibet Regional Banking Regulatory Commission, People’s Daily reported. At the Fifth Central Working Conference on Tibet in 2010, the central government introduced a set of policies of helping Tibet build its own regional commercial bank, in order to ensure leapfrog social and economic development as well as maintain peace and stability in the region.”[3]

Bank of Tibet is another funnel for Beijing to pour in money to obtain its desired result: a Tibet with Chinese characteristics. CGI has happily swallowed from this funnel, knowing it could hardly ask its shareholders to finance a massive capital expenditure on upscaling Gyama, at the very time Chinese rare earth producers are scaling back production, in the hope of reviving falling prices.

When the minerals cycle ticks up again, as it will, Tibetans may need friends worldwide. But because China reserves the mining of Tibet for itself, with very little international investment, what traction do Tibet’s friends worldwide have?

Here again things have moved on since that 2013 book. Not only are Chinese and Canadian miners doing deals to take over each other’s assets, so too the global minerals commodity traders are buying into a slice of the action in China. Specifically, the Swiss commodities trader Trafigura has bought 30 per cent ownership of Jinchuan’s new copper smelter –Jinchuan’s other smelter, the one that didn’t have the oxygen problem and the four months of force majeure contract repudiation. Jinchuan would like to believe it has done Trafigura a favour by giving it access to Chinese markets, but, given chronic over supply, it is Trafigura, able to sell the new smelter’s output into other Asian countries, that is helping out Jinchuan. That new smelter, a big one, is also in a minority nationality area, in Guangxi province.

Jinchuan, the owner of the Shetongmon mine near Shigatse, may also hope that its connection with Trafigura gives it (and China) entrée to the world of commodities futures, hedging, arbitraging and financialisation of minerals. China wants to get into the big league worldwide. Trafigura, however, probably knows how much reputation affects stock prices, and how much a brand can be damaged by hanging out with the wrong crowd.

Some books age gracefully, others quickly wrinkle. When I was completing the manuscript of Spoiling Tibet: China and Resource Nationalism on the Roof of the World three years ago, I knew it would be out of date soon. A snapshot of mining, right across the Tibetan Plateau, is bound to fade, superseded by events. But I wasn’t ready for how fast that book, published less than two years ago, would be out of date, not only about details but about its main argument.

Zed Books gave me the title when they commissioned me to write the book, part of their Asian Arguments series. That title meant I had to take a stand, by the last chapter, as to whether Tibet was indeed spoiled. Along the way I had collected evidence aplenty of rapacious mining, especially a rush for alluvial gold that had definitely despoiled rivers, riverbanks, pastures and even killed sheep and yaks, due to the indiscriminate use of mercury by “artisanal” miners. But Tibet is a big land, a vast island in the sky, close to two percent of the land surface of the planet, and large-scale, intensive deep mining was only just getting under way.

So I eventually declared myself, in line with the present tense of the title, saying Tibet was not yet spoiled, but soon would be. The big mines, with big impacts, were being developed fast, an archipelago of gold/silver/copper/molybdenum mines along the Yarlung Tsangpo, the Kyichu above Lhasa, and around Yulong, in Kham, between Chamdo and Derge. These were all modern, large-scale, capital-intensive mines capable of mining millions of tons of rock a year, something Tibet has never seen, except in the heavily industrialised Tsaidam basin of Amdo.

Hardline meltdowners criticised me for saying Tibet was not yet spoiled. After all the conventional exile narrative has long been that China has raped Tibet nonstop for decades. I thought that an exaggeration, but I was not hopeful. By 2015 or 2016, I reasoned, the pace of big mine construction will have peaked, and once massive capital expenditure has been sunk into mines, rock crushers, ore concentrators, smelters, hydro dams to ensure power supply and all ancillary urbanised workforce facilities, mining must go ahead, if only to service the sunk capital. If Tibet was not yet spoiled, the day would soon come.

Wrong, wrong, wrong. How different things look now. Copper demand has fallen so sharply that copper mines worldwide, including Chinese-owned ones, are being mothballed, in the hope that reduced production might drive prices back up. For Tibet, copper is the key. All the big deposits are basically copper deposits with tiny amounts of gold and silver also recoverable in the same process of crushing the rock to powder, cooking it chemically in concentrators, then finally smelting it, which separates the molten metals. All these deposits also contain the valuable metal molybdenum, or lead and zinc as well.

Back in 2013, the global “supercycle” of high prices for all commodities, especially metals, had been at full speed for over a decade. Even the global financial crisis of 2008-9 caused little more than a blip in demand. The conventional wisdom was that China still has far to go before its wealth, and intensity of resource consumption gets anywhere close to the rich countries it intends to join, so the long term picture is full steam ahead. How wrong we all were, though the resource economists still cling to their graphs showing that per capita the Chinese still use far less copper than, say, Americans. Over the long run, they may yet be right.

But for the foreseeable future, the commodities supercycle is gone, China suffers such overcapacity in smelting metals that much of the money invested in smelters is turning into bad debt. Buying up stockpiles of metals such as copper, when prices are low, long ago ran out as a driver of demand. Copper was further tainted when it emerged that the Chinese warehouses stockpiling coper were using their holdings as collateral to borrow huge amounts to speculate on the overheated real estate market, then on an overheated stock market, often using the same quantum of copper over and over as collateral for loans from different borrowers. This massive scam resulted in a scramble by lenders to find their actual copper in actual warehouses, and make sure it was theirs and not hypothecated to others.

So the big mines that in 2013 looked like they would soon swing into full production –Shetongmon, Gyama, Yulong- slowed right down. Around the world, China is sitting on copper deposits whose deposits are fully mapped, whose mining schedule has been run through endless computer modelling, whose infrastructure is fully planned; and they sit idle. This is what has saved Tibet from being spoiled, past tense.

The pause in completing construction of the big mines may not last. CGI is a sign that China is pressing ahead, even if it makes little business sense.

[1] CBRC Gives Nod to Bank of Tibet, SinoCast Banking Beat, 25 July 2011, www.yicai.com

[2] Ni 43-101 Technical Report – Jiama Phase 2 Expansion Project Mineral Resources & Reserves, For

China Gold International, Mining One, p 169; available online: http://www.chinagoldintl.com/_resources/feasibility_study_jiama.pdf

[3] Bank of Tibet receives business license in China’s Tibet Autonomous Region, China Economic Review, 17 January 2012